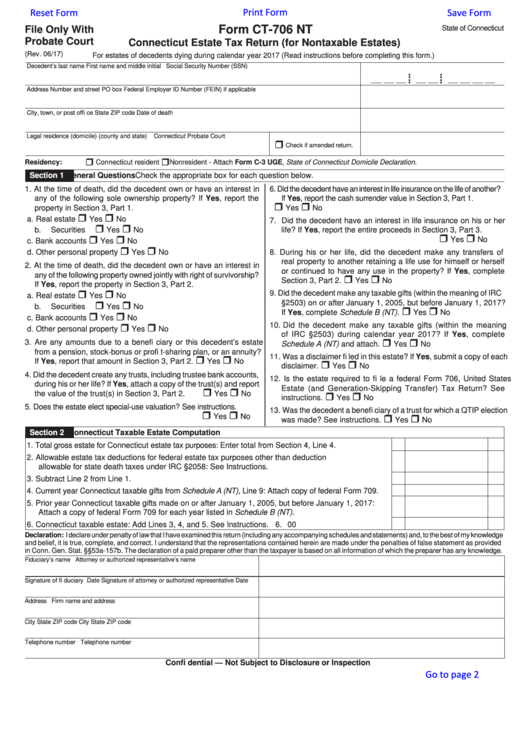

Form Ct 706 Nt

Form Ct 706 Nt - Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this. • each decedent who, at the time of death, was a connecticut resident; Therefore, connecticut estate tax is due from. • for each decedent who, at the time of death, was a nonresident. For each decedent who, at the time of death, was a nonresident of. For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million.

Each decedent who, at the time of death, was a connecticut resident; • each decedent who, at the time of death, was a connecticut resident; For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. 2021 connecticut estate tax return (for nontaxable estates) instructions. Therefore, connecticut estate tax is due from.

2021 application for extension of time for filing. Web 8 rows revised date. • each decedent who, at the time of death, was a connecticut resident; For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this.

Fillable Form Ct706 Nt Connecticut Estate Tax Return (For Nontaxable

• each decedent who, at the time of death, was a connecticut resident; 2021 application for extension of time for filing. Web 8 rows revised date. • for each decedent who, at the time of death, was a nonresident Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this.

Ct 706 Nt 20202021 Fill and Sign Printable Template Online US

Web where applicable, the code will link directly to information on the type of probate matter associated with the form. Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this. • for each decedent who, at the time of death, was a nonresident. 2021 application for extension of time.

Form Ct 706 Nt Ext ≡ Fill Out Printable PDF Forms Online

Web where applicable, the code will link directly to information on the type of probate matter associated with the form. For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. 2021 application for extension of time for filing. For each decedent who, at the time of death, was a nonresident of. Connecticut.

Form 706 Fill out & sign online DocHub

• for each decedent who, at the time of death, was a nonresident. 2021 connecticut estate tax return (for nontaxable estates) instructions. 2021 application for extension of time for filing. Web where applicable, the code will link directly to information on the type of probate matter associated with the form. Web form ct‐706 nt must be filed for:

Fillable Form Ct706 Connecticut Estate Tax Return printable pdf download

For each decedent who, at the time of death, was a nonresident of. Web where applicable, the code will link directly to information on the type of probate matter associated with the form. 2021 application for extension of time for filing. Therefore, connecticut estate tax is due from. Web form ct‐706 nt must be filed for:

Form CT706 NT Download Fillable PDF or Fill Online Connecticut Estate

2021 application for extension of time for filing. Web where applicable, the code will link directly to information on the type of probate matter associated with the form. For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. 2021 connecticut estate tax return (for nontaxable estates) instructions. Therefore, connecticut estate tax is.

2007 Form CT DRS CT706 NT Fill Online, Printable, Fillable, Blank

2021 application for extension of time for filing. Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this. • each decedent who, at the time of death, was a connecticut resident; Web 8 rows revised date. Web form ct‐706 nt must be filed for:

Form Ct 706 Nt - • each decedent who, at the time of death, was a connecticut resident; Web 8 rows revised date. Web where applicable, the code will link directly to information on the type of probate matter associated with the form. • for each decedent who, at the time of death, was a nonresident. Web form ct‐706 nt must be filed for: 2021 application for extension of time for filing. Therefore, connecticut estate tax is due from. For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. • for each decedent who, at the time of death, was a nonresident For each decedent who, at the time of death, was a nonresident of.

• each decedent who, at the time of death, was a connecticut resident; • for each decedent who, at the time of death, was a nonresident Web form ct‐706 nt must be filed for: Therefore, connecticut estate tax is due from. Each decedent who, at the time of death, was a connecticut resident;

For decedents dying on or after january 1, 2011, the connecticut estate tax exemption amount is $2 million. Each decedent who, at the time of death, was a connecticut resident; Web where applicable, the code will link directly to information on the type of probate matter associated with the form. Connecticut estate tax return (for nontaxable estates) for estates of decedents dying during calendar year 2022 (read instructions before completing this.

Web form ct‐706 nt must be filed for: Web 8 rows revised date. • for each decedent who, at the time of death, was a nonresident

Web 8 rows revised date. Therefore, connecticut estate tax is due from. 2021 connecticut estate tax return (for nontaxable estates) instructions.

Connecticut Estate Tax Return (For Nontaxable Estates) For Estates Of Decedents Dying During Calendar Year 2022 (Read Instructions Before Completing This.

2021 connecticut estate tax return (for nontaxable estates) instructions. • each decedent who, at the time of death, was a connecticut resident; Web form ct‐706 nt must be filed for: Web 8 rows revised date.

• Each Decedent Who, At The Time Of Death, Was A Connecticut Resident;

Each decedent who, at the time of death, was a connecticut resident; • for each decedent who, at the time of death, was a nonresident. For each decedent who, at the time of death, was a nonresident of. Therefore, connecticut estate tax is due from.

For Decedents Dying On Or After January 1, 2011, The Connecticut Estate Tax Exemption Amount Is $2 Million.

• for each decedent who, at the time of death, was a nonresident 2021 application for extension of time for filing. Web where applicable, the code will link directly to information on the type of probate matter associated with the form.